策略靈感來源從以下這個影片來的,可以先看看

看完後,有點好奇績效是不是真的那麼厲害,嘗試改成XQ的交易程式碼,跑出來的績效似乎還不錯,2016/09到2021/10,獲利接近160萬,最驚人的是勝率竟然高達81.08%,整個權益曲線也算是一路向上,仔細的看了下,最大虧損交易竟然是-31萬,最大區間虧損也高達-62萬,嗯,這應該不是普通人能用的策略~~

既然上面的結果不是普通人能用的,那就只好繼續來改造下,看能否搞出個普通人能用的策略,運氣還不錯,同樣回測區間,也能獲利136萬,雖然勝率變低,但最大虧損跟最大區間虧損,大幅降低至5.8萬跟13萬,且權益曲線是一路往上,每年都是獲利的,已經算是不錯的策略了

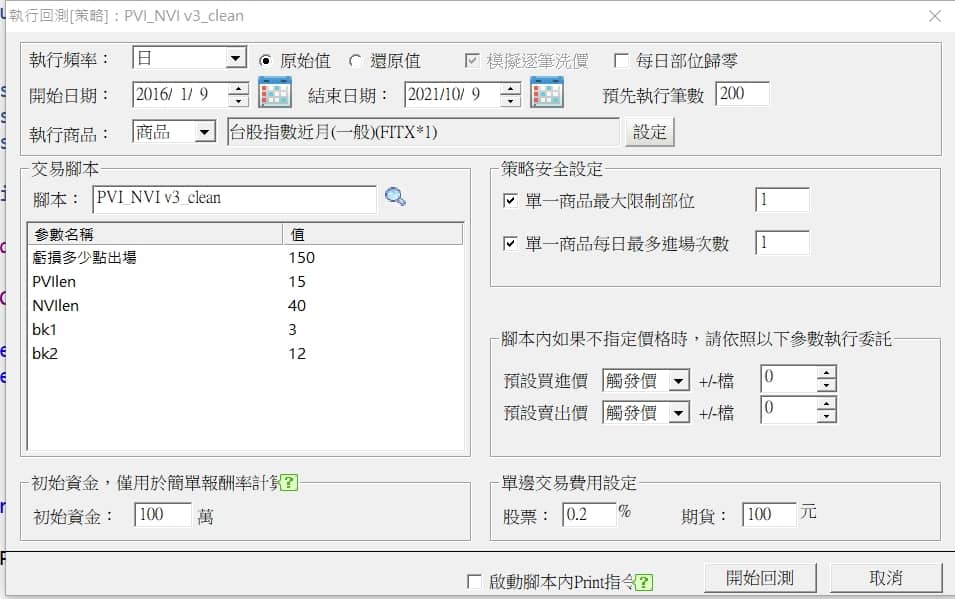

回測設定如下,有興趣的可以調整參數或是增加其他進出場條件,應該能找到更加的組合。

檔案下載

程式碼如下

//https://www.youtube.com/watch?v=TpR7Cdy7pko

//v3 增加出場濾網,不然MDD太大

input: lostex(150,"虧損多少點出場");

input: PVIlen(15),NVIlen(40),bk1(3),bk2(12);

vars: avPVI(0), avNVI(0);

vars: trendbull(false),trendbear(false);

vars: intrabarPersist entryonce(0);

Variable: _pvi(1),_nvi(1);

if date<>date[1] then entryonce=0;

If CurrentBar = 1 then

_pvi = 100

else

begin

if Volume > Volume[1] then

_pvi = _pvi[1] + ((Close - Close[1]) / Close[1])*_pvi[1]

else

_pvi = _pvi[1];

end;

avPVI=average(_pvi,PVIlen);

If CurrentBar = 1 then

_nvi = 100

else

begin

if Volume < Volume[1] then

_nvi = _nvi[1] + ((Close - Close[1]) / Close[1])*_nvi[1]

else

_nvi = _nvi[1];

end;

avNVI=average(_nvi,NVIlen);

trendbull=_nvi>avNVI and _pvi<avPVI;

trendbear=_nvi>avNVI and _pvi>avPVI;

if position<=0 and trendbull and entryonce=0

// and close>average(getfield("close","D")[1],5) 測試用條件

and close>highest(high[1],2) then begin

setposition(1,highest(H,bk1));

entryonce=1;

end;

//if position>=0 and trendbear then //翻單

// setposition(-1,lowest(l,bk2));

if position>=0 and filled=1 and trendbear then begin

setposition(0,market);

end;

if position>=0 and filled=1 and close<filledavgprice-lostex then begin

setposition(0,market);

end;

//-----期貨換月出場

var: b_balanceDay(false);

if date<>date[1] then begin

b_balanceDay=false;

if (dayofmonth(Date)>=15 and DayofMonth(Date)<=21 and DayofWeek(Date)=3) then b_balanceDay=true;

end;

if b_balanceDay=true and position=1 and filled=1 and time>=130000 then begin

setposition(0,close);

end;

![[VIP] XQ版RS相對強弱PR指標](https://cdn.aplus.trading/wp-content/uploads/2024/11/a-captivating-illustration-of-the-relative-strengt-t0oo_72pQ6-5mpJuqSoDQ-h1cSwJr9Qv-Gwfy41ebhgw-870x570.jpeg)

By

By![[VIP]用彼得林區邏輯 + XQ 選股中心打造成長型策略](https://cdn.aplus.trading/wp-content/uploads/2025/07/a-captivating-modern-digital-illustratio_7OaYIF8kT4aUUDGs6AJjBw_tLDjMWjvSXWPG5ycIUliAg-870x570.jpeg)

By

By

By

By![[VIP] 達人Alan分享的基本面策略](https://cdn.aplus.trading/wp-content/uploads/2026/05/cover-870x570.jpg)

![[VIP] 年年獲利的處置股策略](https://cdn.aplus.trading/wp-content/uploads/2026/05/makemoney-150x150.jpg)

![[VIP] 五年報酬率200%+的委買策略](https://cdn.aplus.trading/wp-content/uploads/2026/04/委買-150x150.jpg)

第41,42行不論多空的判斷條件都是_nvi>avNVI,似乎不太對?

請問影片連結還有嗎?

已修正

不用理會前一篇找影片連結的留言, 有找到了

但丟進回測, 一樣的條件跑出來的結果天差地遠, 包括VIP的也是, 不知道問題出在哪

策略開發出來,本就無法保證未來績效,這篇文章是2022/02寫的,後來的確表現沒那麼好,您的回測應該是最近幾年,所以回測結果一定跟上面不同,如遇到後期表現不佳,可以嘗試再優化看看,不過這個策略近期似乎又要創高了,可以再觀察看看

另外,建議是測試下面的VIP策略,表現的是比較好的,202305寫的,一直到202410都在創高,最近沒創高,但也沒啥回檔

https://aplus.trading/原創-這簡單也行pvi均線黃金交叉策略-vip/